W2 - CPI Inflation Decelerates For 6th Straight Month, Microsoft Investing $10B Into OpenAI, Layoffs Announced By Goldman Sachs & Coinbase, Tesla Cuts Prices, and TSMC + Delta + JPMorgan Earnings

Consumer prices fell 0.1% in December and rose 6.5% for the year, in line with expectations. This reading marks the sixth consecutive report with decelerating inflation. Excluding food and energy, core CPI rose 0.3% as services inflation continues to remain sticky. Here’s the breakdown:

Microsoft to invest $10B into OpenAI, the creator of ChatGPT, at a $29B valuation. Microsoft would reportedly get 75% of OpenAI’s profits until it makes all of its investment back, after which the company would own a 49% stake.

Goldman Sachs is laying off over 3kemployeesin the company’s largest restructuring since the Great Financial Crisis of 2008. IPO issuance and M&A deal volume plunged 94% last year due to the suddenly inhospitable markets.

Wells Fargo is stepping back from the housing market amid regulatory pressure and the impact of higher interest rates, despite being one of the largest players in the space. Executives noted that the shift will result in a fresh round of layoffs for the bank’s mortgage operations.

JPMorgan sues withfrank.org founder for fraudafter she allegedly created over four million fake accounts on the student aid platform before selling the site to JPMorgan for $175m in September 2021.

Lucid produced more vehicles than expected this yearas the company quickly ramps up its output. Q4 volume expanded 53% vs the previous quarter. The report shows 7,180 completed vehicles vs guidance for 6K - 7K.

Rest of World 🌏

China reports massive increase in COVID deaths after the WHO criticized Beijing for its lack of transparency. China said nearly 60,000 people with COVID-19 had died in hospitals since it abandoned its zero-COVID policy last month.

China’s inflation gauges show heightened price pressureas the economy deals with the reopening. Consumer prices came in hotter than expected, rising 1.8% for the year. Meanwhile, wholesale deflation eased to 0.7% in December from 1.3% in the previous month.

Consumer inflation in Japan’s capital hits 4%, above consensus expectations of 3.8% and marking the 7th straight month above the BoJ’s target. Core CPI rose 2.7% and accelerated its pace of gain.

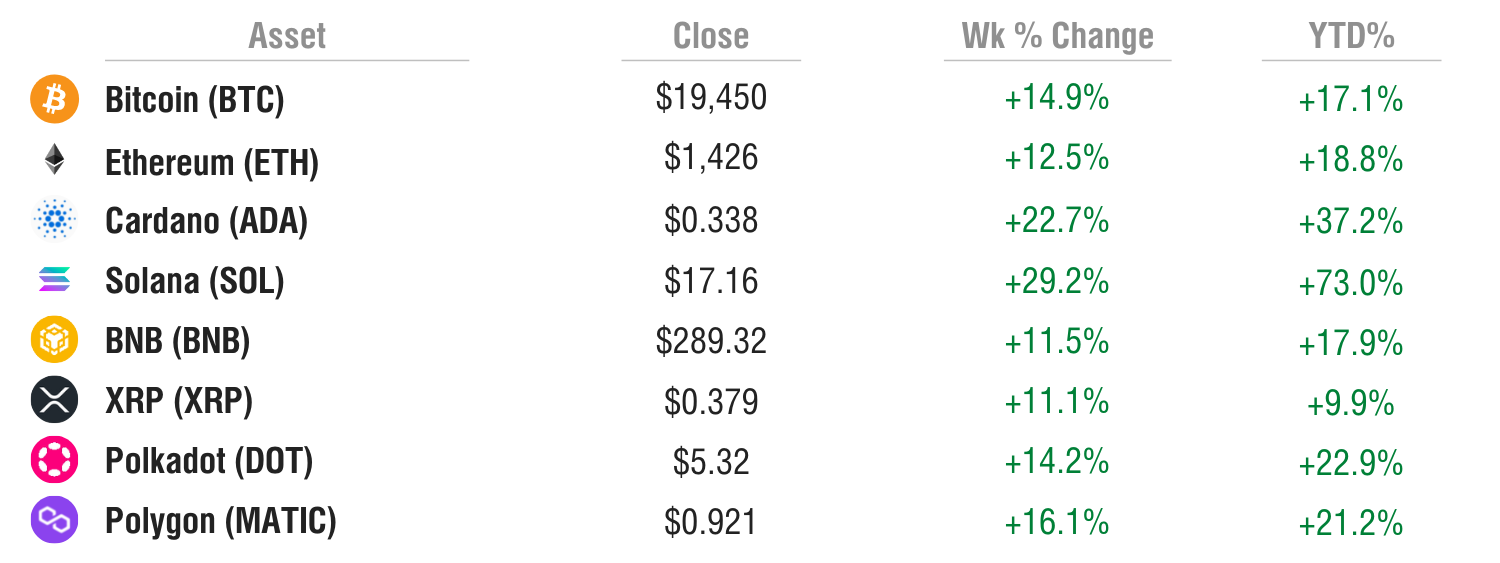

Crypto ⚡

Coinbase to slash another 20% of its workforce after already cutting 18% back in June. The company expects a $500m EBITDA loss this year but says the layoffs will help reduce operating expenses by 25% in Q1.

Crypto.com also cuts 20%of its staff as the industry continues to deal with lower transaction volume and other effects of the ongoing crypto winter. Crypto.com has seen its CRO token drop by nearly 96% this year.

FTX has recovered $5B of liquid assets including cash, crypto, and other securities. FTX’s new CEO, John J. Ray, previously attested that at least $8 billion of customer assets were unaccounted for.

Binance plans a 15-30% hiring spreein 2023, despite the dramatic crypto downturn. Quite a contrarian move considering this comes just weeks after its competitors Coinbase, Huobi, and Kraken all announced 20% RIFs or greater.

SMM Product Hunt 🧠

Dilutional.com is a promising new tool that can help you be more successful in the stock market. Their algorithm and the data that they provide takes a lot of the complexity out of trading.

The features they offer include access to market data, live charts, pattern and trend recognition, instant alerts, direct access to press releases, and stock price predictions.

The stock prediction tool uses different algorithms to predict a stock’s downfall, giving you advance warning to help prevent losses or provide opportunities to short with a higher conviction.

Trading in US markets can be extremely complex, but incorporating this tool into your strategy could greatly increase your chances of success and savetime in the process.

The product is currently in private beta, but expected to launch this year. The pricing and exact launch date have yet to be revealed, but you can join their waitlist today to be eligible for a free trial and get notified of when they launch.

We’d love to hear your thoughts about SMM. Click here to give feedback.

Want to partner with Sunday Morning Markets? Click hereto inquire.

All content provided by Sunday Morning Markets is for informational and educational purposes only and is not meant to represent trade or investment recommendations.