Weekly Financial Market Insights 📈

Fed Minutes Give Dovish Sentiment To Markets, US Economic Activity Contracts, Bob Iger Back As Disney CEO, HP To Layoff ~5K Employees, and Dell + Zoom + Autodesk + Best Buy Earnings

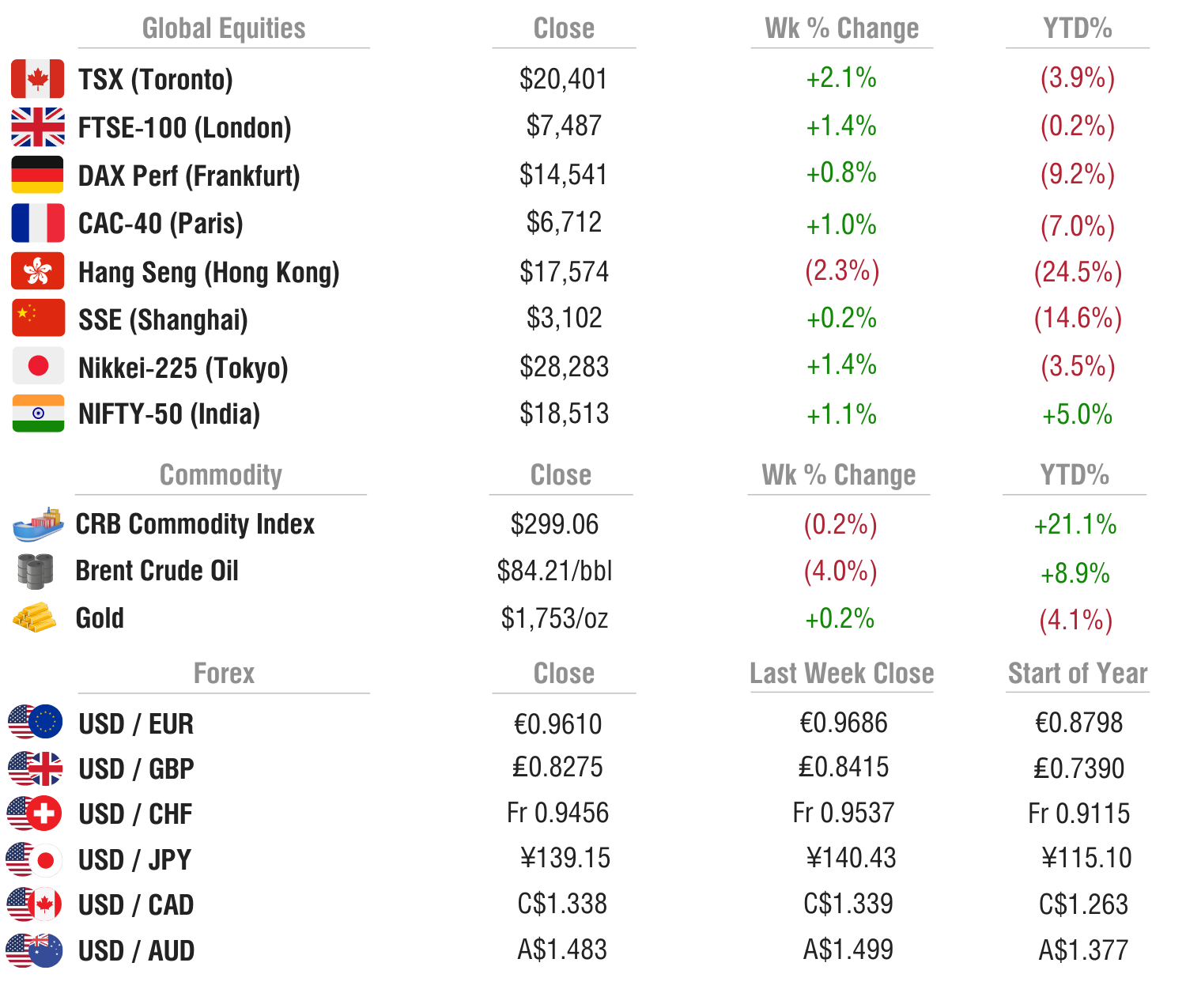

Sunday Morning Markets ☕

Trading Week 47, covering Monday, Nov 21 through Friday, Nov 25. Your weekly financial markets update, in less than 5 minutes.

The Week In Review ⏪

Markets closed early on Friday at 1 PM ET, and all of Thursday for Thanksgiving.

Fed Meeting Minutes give dovish relief to markets, “slowing in the pace of increase would likely soon be appropriate”.

More layoffs this week with HP, Carvana, and others announcing new RIFs.

Bob Iger is coming back as CEO of Disney.

US economic contraction has worsened so far in November, S&P PMI shows.

German wholesale prices fell 4.2% during the month of October.

Grayscale’s Bitcoin Trust ($GBTC) now trades at a 45% discount to NAV.

US Markets 🇺🇸

Fed officials see smaller rate hikes ahead, minutes show. “A substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate,” causing stocks to rally on Wednesday.

U.S. economic activity continues to contract this month as the first reading for the S&P Manufacturing PMI came in at 46.3, well below estimates of 49.5 and down from 48.2 in October. "Companies are reporting increasing headwinds from the rising cost of living, tightening financial conditions”

Bob Iger named Disney CEO again after the board received internal complaints from senior leadership that Bob Chapek was not fit for the job. Iger has agreed to serve as CEO through the end of 2024 and will earn a $1m base annual salary.

HP to lay off 4K to 6K employees over next three years after the company reported weakness in commercial and consumer PC sales. The company said the plan should result in annualized gross run rate savings of $1.4 billion or more.

Initial jobless claims jump to 240K, the highest since August, and above the consensus estimate of 225K. The number of people already collecting jobless benefits rose by 48K to 1.55m, the highest level in eight months.

New home sales unexpectedly jump in October despite high mortgage rates. Sales rose 7.5% to a seasonally-adjusted annual rate of 632K in October, up from 588K in the prior month and well above estimates of 570K.

Rest of World 🌏

Euro zone economic activity contracted for fifth straight month, adding to fears of a recession. The S&P Eurozone composite PMI rose to 47.8 in November, up from 47.3 in October but still in negative territory.

German producer prices fell unexpectedly in October, dropping 4.2% during the month, compared with expectations for a rise of 0.9%. ECB President Christine Lagarde noted that interest rates will need to be continuously lifted to levels that restrict economic expansion in order to combat inflation.

Beijing announces COVID lockdowns as more and more apartment compounds forbid residents from leaving for multiple days. “You constantly hear of someone going into lockdown and you have this constant feeling that you’re going to be next.”

Crypto ⚡

Grayscale won’t share proof of reserves due to “security concerns” as their highly traded Bitcoin trust ($GBTC) trades at a 45% discount to NAV. Investors continue to price in counter-party risk as Digital Currency Group, the parent of Grayscale, also owns the recently troubled Genesis Capital.

FTX hacker moved $200m to 12 wallets on the same day the crypto exchange filed for bankruptcy protection. Blockchain experts argued that the looter was likely an insider who had access to the exchange's cold wallets. The FTX exploiter moved a total of 180,000 ETH to 12 wallets.

US Senators ask Fidelity to reconsider Bitcoin 401(k) offerings following FTX collapse. The U.S. financial services firm allows companies to offer their digital assets account as part of their 401(k) lineup.

Binance allocates another $1B to recovery fund, effectively increasing the size of the fund to over $2 billion. Aptos Labs and Jump Crypto joined Binance's initiative and will contribute $50 million to the fund.

SMM is powered by

🧑💻 Alpha Vantage provides enterprise-grade financial market data through a set of powerful and developer-friendly APIs. From traditional asset classes (e.g., stocks and ETFs) to economic metrics, from foreign exchange rates to cryptocurrencies, from fundamental data to technical indicators, Alpha Vantage is your one-stop shop for real-time and historical global market data delivered through RESTful stock APIs, Excel, and Google Sheets.

Earnings Reports 💰

Dell Technologies ($DELL) — View report

Revenue: $24.72B vs $24.61B expected and $26.42B year ago (-6% YoY)

Adjusted EPS: $2.30 vs $1.61 expected and $1.66 year ago (+39% YoY)

Segment Breakdown:

Infrustructure Solutions: $9.63B vs $8.56B year ago (+12% YoY)

Client Solutions: $13.78B vs $16.56B year ago (-17% YoY)

Other: $1.31B vs $1.31B year ago (+0% YoY)

Guidance: Guidance given on earnings call.

Market Reaction (24hrs after report): +6.8%

—

Zoom Technologies ($ZM) — View report

Revenue: $1.1B vs $1.1B expected and $1.05B year ago (+5% YoY)

Adjusted EPS: $1.07 vs $0.84 expected and $1.11 year ago (-4% YoY)

Free Cash Flow: $273m vs $375m year ago (-27% YoY)

Important Notes: Customers contributing over $100K TTM up 31% YoY to 3,286. Enterpise client base +14% YoY to 209,300.

Guidance for Q4:

Sales of $1.095B - $1.105B

Non-GAAP EPS of $0.75 - $0.78

Market Reaction (24hrs after report): -3.9%

—

Best Buy ($BBY) — View report

Revenue: $10.6B vs $10.3B expected and $11.9B year ago (-11% YoY)

Adj EPS: $1.38 vs $1.02 expected and $2.08 year ago (-34% YoY)

Segment Breakdown:

Domestic: $9.8B, down 11% YoY

International: $0.8B, down 15% YoY

Guidance: Raised FY22 sales forcast -3% to -1.5% comparable sales and adjusted EPS of $11.50 to $12.10.

Market Reaction (24hrs after report): +12.7%

—

AutoDesk ($ADSK) — View report

Revenue: $1.3B vs $1.3B expected and $1.1B year ago (+14% YoY)

Adjusted EPS: $1.70 vs $1.70 expected and $1.34 year ago (+27% YoY)

Segment Breakdown:

Arch, Eng, Cons (AEC): $575m, up 13% YoY

AutoCAD: $354m, up 10% YoY

Manufacturing (MFG): $254m, up 13% YoY

Media and Ent. (M&E): $78m, up 24% YoY

Other: $19m, up 138% YoY

Guidance for Q4: Sales of $1.3B - $1.32B and adjusted EPS $1.77 - $1.83

Market Reaction (24hrs after report): -5.8%

—

Other Reports:

Week Ahead 📅

Monday

US - Dallas Fed Manufacturing Index (Nov) 🇺🇸

Tuesday

Canada - GDP Growth Rate (Q3) 🇨🇦

Germany - Inflation Rate (Nov) 🇩🇪

China - NBS Manufacturing PMI (Nov) 🇨🇳

Earnings Reports: Intuit, Workday, Crowdstrike, NetApp, Bilibili💰

Wednesday

US - GDP Growth Rate (Q3) 🇺🇸

US - ADP Employment Change (Nov) 🇺🇸

US - JOLTS Job Openings (Oct) 🇺🇸

EU - Inflation Rate (Nov) 🇪🇺

France - Inflation Rate (Nov) 🇫🇷

Italy - Inflation Rate (Nov) 🇮🇹

Earnings Reports: Salesforce, Synopsys, Snowflake, Hormel Foods, Splunk, Five Below, Okta, XPeng 💰

Thursday

US - Personal Income & Spending (Oct) 🇺🇸

US - ISM Manufacturing PMI (Nov) 🇺🇸

EU - Unemployment Rate (Oct) 🇪🇺

Japan - Consumer Confidence (Nov) 🇯🇵

Earnings Reports: Toronto Dominion Bank, Dollar General, Marvell Technology, Veeva Systems, Ulta, Zscaler, UiPath, Samsara, ChargePoint, Asana 💰

Friday

US - Nonfarm Payrolls (Nov) 🇺🇸

US - Unemployment Rate (Nov) 🇺🇸

Canada - Unemployment Rate (Nov) 🇨🇦

Did you like this Sunday Market Newsletter? Consider sharing it!

We’d love to hear your thoughts about SMM. Click here to give feedback.

Want to partner with Sunday Morning Markets? Click here to inquire.