Weekly Financial Market Insights 📈

Trading Week 33 ... Wayfair, Peloton Layoffs, Acala Stablecoin Hacked, US Manufacturing & Housing Data, and Walmart + Home Depot + Target Earnings

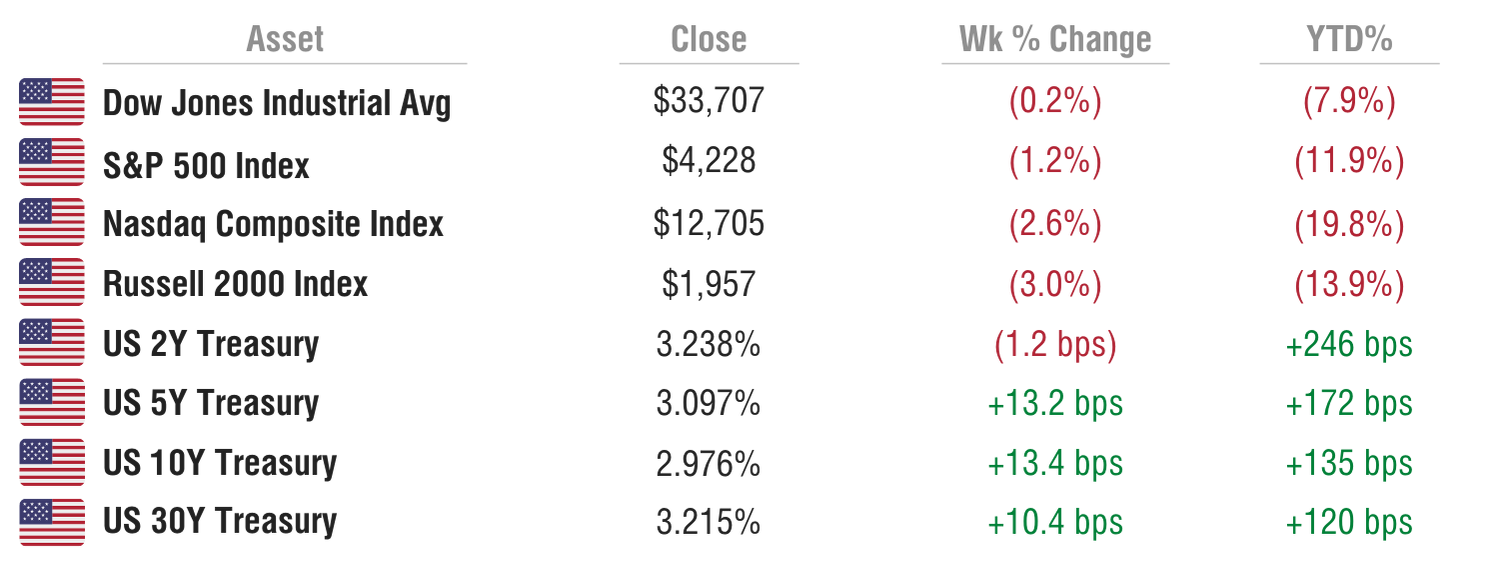

Sunday Morning Markets ☕

Your weekly financial markets update, in less than 5 minutes. Market coverage for Monday, August 15 - Friday, August 19.

Last Week ⏪

US equities take a breather after rallying for four straight weeks. Layoffs continue with Wayfair & Peloton falling as the next victims, new economic and housing data continue to show weakness, inflation skyrockets in Europe — all that and more in this week of Sunday Morning Markets…

US Markets 🇺🇸

CB Leading Economic Index falls 0.4% marking its fifth consecutive monthly decline and signaling a higher risk of a recession in the near term. “The Conference Board projects the US economy will not expand in the third quarter and could tip into a short but mild recession by the end of the year or early 2023.”

Empire State manufacturing plunges to -31.3 in August, signaling a deep contraction in economic activity. New orders fell to -29.6, a level only seen in 2008 and 2020.

Philly Fed Manufacturing Index stronger than expected in first August print as general activity index jumps 19 points to a +6.2 reading. Economists were expecting only a 7-point jump to a -5 reading.

Amazon hikes FBA fees for the holidays as it battles rising delivery and fulfillment costs. U.S. and Canadien sellers will now pay a $0.35 fee for every item sold between October 15th and January 14th of next year.

Homebuilders say housing is in a recession as Wells Fargo Housing Market Index dropped six points in August to a reading of 49, the index’s eighth consecutive decline. Sales conditions fell to 57, sales expectations fell to 47, and buyer traffic fell to 32.

Home buyers are backing out of deals at staggering rates according to Redfin’s latest report. 63,000 home purchases were canceled in July, representing over 16% of homes under contract at the time.

Wayfair ($W) lays off ~900 employees as they react to lower sales forecasts. "This year, growth has not materialized as we had anticipated. Our team is too large for the environment we are now in, and unfortunately, we need to adjust."

Peloton ($PTON) lays off another 780 jobs and shuts down a significant number of retail stores. The company also announced they will be raising prices for their products and shifting to 3rd party delivery services in an effort to rebalance margins.

Rest of World 🌏

China surprises markets with rate cuts after economic data shows a significant slowdown. Retail sales, industrial output, and investment all slowed and missed economists’ estimates in July. China’s central bank cut both one-year and seven-day lending rates by 10 basis points.

Germany’s producer prices jump 37.2% from previous year and 5.6% from June. Energy prices were the primary catalyst for the large inflation print, surging 105%. Excluding energy, producer prices were 14.6% higher.

UK inflation hits double digits as prices rose 10.1% in July, well above estimates of 9.8% and a significant jump from the 9.4% inflation seen in June. Meanwhile, real wages in the UK fell by 3% in the second quarter. The Bank of England expects inflation to top out at 13.3% in October.

Putin to deepen their relationship with North Korea after sending Kim Jong Un a congratulatory telegram on North Korea’s Liberation Day. Putin expressed interest in “continuing to expand the comprehensive and constructive bilateral relations” between Russia and North Korea.

Five Chinese companies delist from NYSE with a timeline for the end of August. China Life Insurance, PetroChina, Sinopec, Aluminum Corporation of China, and Sinopec Shanghai Petrochemical all announced they would be “voluntarily delisting” due to the high administrative burden induced by NYSE. The news comes as the Securities and Exchange Commission increases its scrutiny of Chinese companies' audits.

Europe eyes SpaceX as a replacement for Russian rockets as the Ukraine conflict has blocked western access to Russia’s Soyuz rockets. The European Space Agency began preliminary technical discussions with Elon Musk’s SpaceX that could lead to the temporary use of its launchers.

Crypto ⚡

Acala’s Stablecoin drops 99% after hackers issue 1.3B tokens by exploiting a bug in the protocols liquidity pool. The Polygon-based stablecoin aUSD plunged from roughly $1.03 per token to $0.009.

Celcius has a $2.8B hole in its balance sheet and is on pace to run out of cash by October, a court filing reveals. The filing, submitted to the U.S. Bankruptcy Court of New York shows the lender holds $2.8 billion less in crypto than it owes to depositors.

CME expands crypto offerings with options for Ether. The exchange plans to allow traders to make bets on ETH and hedge risks ahead of the Ethereum merge. The ETH options are expected to launch on September 12th.

This newsletter is brought to you by:

🚀 Alpha Tournament: @nyc10022 is in the lead after the first week of Season 13’s competition. Don’t forget to save your seat for next season!

—

🧑💻 Alpha Vantage provides enterprise-grade financial market data through a set of powerful and developer-friendly APIs. From traditional asset classes (e.g., stocks and ETFs) to economic metrics, from foreign exchange rates to cryptocurrencies, from fundamental data to technical indicators, Alpha Vantage is your one-stop shop for real-time and historical global market data delivered through RESTful stock APIs, Excel, and Google Sheets.

Earnings Reports 💰

Nu Holdings ($NU)

Revenue: $1.2B vs $1.04B expected and $0.34B year ago (+244% YoY)

Gross Profit: $364M vs $166M year ago (+119% YoY)

Gross Profit Margin: 31.4% vs 49.5% year ago (-1810 bps YoY)

Adjusted Net Income: $17M vs -$16.5M year ago

Guidance: No guidance provided.

Important Notes: Added 5.7M new customers during the quarter, bringing their total to 65.3M (+57% YoY). Average Revenue per Active Customer (ARPAC) grew 105% over the year to $7.80/mo while the average cost to serve an active customer stayed flat around $0.80/mo.

Market Reaction (24hrs after report): +18%

—

Revenue: $152.9B vs $150.8B expected and $141.0B year ago (+8.4% YoY)

EPS: $1.77 vs $1.62 expected and $1.78 year ago (-0.6% YoY)

Op. Income: $6.9B vs $7.4B year ago (-6.8% YoY)

Free Cash Flow (YTD): $1.7B vs $7.4B year ago (-77% YoY)

Guidance: Q3 guidance for 5% sales growth and an 8-10% decline in operating income. Full-year guidance for 4.5% sales growth and an 9-11% decline in operating income.

Important Notes: Same-store sales grew 6.5% over the year, higher than the 5.9% expected by analysts. E-commerce sales grew 12%. Walmart has a glut of inventory, as levels rise 26%. The company “canceled billions of dollars in orders to help align inventory levels with expected demand”.

Market Reaction (24hrs after report): +5.1%

—

Revenue: $43.8B vs $43.4B expected and $41.1B year ago (+6.5% YoY)

EPS: $5.05 vs $4.94 expected and $4.53 year ago (+11.5% YoY)

Op. Income: $7.21B vs $6.64B year ago (+8.6% YoY)

Free Cash Flow (YTD): $5.74B vs $8.91B year ago (-36% YoY)

Guidance: Reaffirmed prior full year guidance of sales growth around 3%, operating margin of 15.4%, and EPS growth in mid-single digits.

Important Notes: Number of customer transactions down 3% from year earlier to 467.4M. Average ticket value rose 9.1% to $90.02, largely due to price inflation. In an earnings call, company said that project backlogs were still healthy despite the weaker housing market.

Market Reaction (24hrs after report): +4.1%

—

Revenue: $2.94B vs $3.03B expected and $2.28 year ago (+29% YoY)

EPS: -$1.03 vs -$1.06 expected and -$0.61 year ago

Gross Profit: $1.1B vs $0.9B year ago (+17% YoY)

Breakdown by Division:

E-Commerce: Rev $1.7B (+51%), Adj EBITDA -$648M(-12%)

Digital Entertainment: Rev $0.72B (-39%), Adj EBITDA +$334M(-55%)

Digital Financial Services: Rev $0.28B (+214%), Adj EBITDA -$111.5M(+28%)

Guidance: Suspended revenue guidance for FY’22 due to macro uncertainties.

Market Reaction (24hrs after report): -14%

—

Revenue: $26.04B vs $26.04B expected and $25.16B year ago (+3.5% YoY)

EPS: $0.39 vs $0.72 expected and $3.65 year ago (-89% YoY)

Gross Profit: $1.1B vs $0.9B year ago (+17% YoY)

Inventory: $15.32B, grew 10% from last quarter and 36% from last year

Guidance: Reiterate full-year guidance of revenue growth in low to mid single digits & operating margin ~6% for second half of year.

Important Notes: Store-comparable sales grew just 1.3% during the year while digital-comparable sales grew 9%. Cash levels of $1.1B, down from $7.4B a year ago.

Market Reaction (24hrs after report): -2.6%

Week Ahead 📅

Monday

Chicago Fed National Activity Index

Earnings Reports: Palo Alto Networks ($PANW), Zoom Communications ($ZM), DLocal ($DLO)

Tuesday

S&P U.S. manufacturing PMI (flash)

S&P U.S. services PMI (flash)

New home sales (SAAR)

Earnings Reports: Intuit ($INTU), Medtronic ($MDT), JD,com ($JD), Pinduoduo ($PDD), XPeng ($XPEV)

Wednesday

Durable goods orders

Core capital equipment orders

Pending home sales index

Earnings Reports: NVIDIA ($NVDA), Salesforce ($CRM), Snowflake ($SNOW), Autodesk ($ADSK), Splunk ($SPLK), NetApp ($NTAP)

Thursday

Jobless claims

Earnings Reports: Toronto Dominion ($TD), Dollar General ($DG), Marvell Tech ($MRVL), Dell Technologies ($DELL), Ulta Beauty ($ULTA), Grab Holdings ($GRAB), Affirm ($AFRM)

Friday

PCE Inflation

Disposable incomes

Consumer spending

UMich consumer sentiment index

Did you like this Sunday Market Newsletter? Consider sharing it!

Until next Sunday…