Weekly Financial Market Insights 📈

Trading Week 32 ...July Inflation Data, Inflation Reduction Act, US Treasury Blacklists Tornado Cash, and Disney + Coinbase + Palantir Earnings

Sunday Morning Markets ☕

Your weekly financial markets update, in less than 5 minutes. Market coverage for Monday, August 8 - Friday, August 12.

Last Week ⏪

Another strong week for US Equities as they continue to rally from the trough seen in the middle of June. Inflation data came in weaker than expected for both the CPI and PPI readings, giving equities another push higher. The S&P500 is now up nearly 17% from the bottom, while the Nasdaq is up over 22%. The question is; have we seen THE bottom, or is this just a bear-market rally?

Elon Musk sells another batch of Tesla shares, Congress passes a massive spending package, the US Treasury blocks Americans from using crypto-mixing service “Torando Cash”, and M&A activity starts to pick up — all that and more in this week of Sunday Morning Markets…

US Markets 🇺🇸

Consumer prices (CPI) rose 8.5% in July, coming in below expectations as energy fell 4.6% during the month. Core-CPI (excluding food and energy) rose 5.9% annually and 0.3% from the month prior. Wages grew 0.5% during the month, adding more upward pressure on inflation.

The Inflation Reduction Act gets passed by the Senate, sending the bill to the Democratic-majority House. Democrats say the Bill will reduce the deficit by over $300B. The Bill includes new spending for climate initiatives, reduction in health care costs, $80B for the IRS, and higher tax rates for corporations.

Elon Musk sells $6.9B in Tesla shares with the fear he may not be adequately capitalized in the event he is forced to buy Twitter. This comes after he said in April that he had no further plans to sell Tesla shares. He also said if he wins the Twitter battle, he would potentially use the money to buy back his shares or start a new social media company.

Producer Price Index (PPI) rose 9.8% annually and declined 0.5% from the month prior. The negative monthly print was led by a 9% drop in wholesale energy prices. Core PPI (excluding food and energy) still saw a 0.2% monthly increase, suggesting prices may still be rising.

Worker productivity drops 4.6% in Q2 after falling 7.4% in Q1, marking the weakest back-to-back drop since 1947. Meanwhile, unit labor costs jumped 10.8% from the year prior, the largest jump since 1982. These rising labor costs suggest sustained upward pressure on inflation.

AppLovin ($APP) submits M&A offer to Unity ($U) valuing Unity at a $20B enterprise value. The all-stock deal would represent a 48% premium for Unity shares at the time of the announcement. This offer puts pressure on Unity’s $4.4B outstanding acquisition deal with Ironsource ($IS).

Amazon ($AMZN) to buy iRobot ($IRBT) for $61/share in an all-cash deal valuing the vacuum-maker at roughly $1.7B. This will mark Amazon’s fourth largest acquisition of all time as the company steps further into the consumer robotics and smart home device space.

Rest of World 🌏

SoftBank posted a $23.4B loss in Q2, becoming the worst quarter in the company’s history. SoftBank’s Vision Fund represented $21.7B of that loss, the second-worst quarter in the Fund’s history. The company also announced a ¥400B ($3B) share buyback program.

Apple asks suppliers in Taiwan to label products “Made In China” in accordance with China’s customs relations. The products can be labeled “Taiwan, China” or “Chinese Taipei”. This news comes after House Speaker Nancy Pelosi’s trip to Taiwan last week.

Canada loses jobs in back-to-back months as the economy continues to slow. According to Statistics Canada, the economy lost 30,600 jobs in July after losing 43,000 jobs in June, much lower than the gain of 15,000 jobs that economists were expecting.

China’s consumer prices hit a multi-year high as the price of pork jumps 20.2% from a year ago. Headline inflation was 2.7% in July, below expectations of 2.9%. Excluding food, consumer prices in China actually declined 0.1% from the previous month.

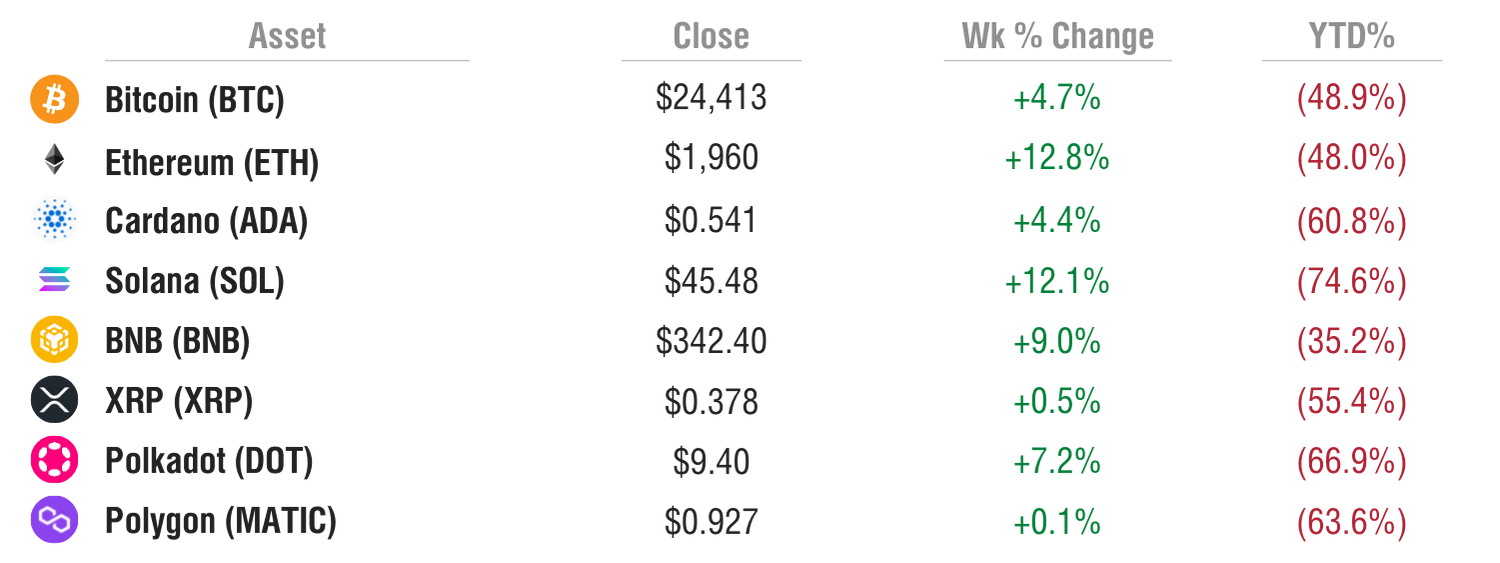

Crypto ⚡

Galaxy Digital ($GLXY.TO) posts a $554.7M loss in Q2 primarily due to the crypto market downturn. The company’s assets under management dropped 40% from the first quarter. CEO Michael Novogratz said, "I don't feel nearly as bad as I thought I would, and I hope it's the worst quarter this firm ever has."

The US Treasury blacklists wallets using Tornado Cash. All Americans are now banned from using the crypto-mixing service which North Korean hackers have allegedly used to launder stolen crypto funds.

Mercado Libre ($MELI) expands crypto trading across LATAM after a successful start in Brazil. Last December the company launched Mercado Pago, a digital wallet enabling users to buy or sell BTC, ETH, and USDP. The application quickly grew to over 1M users in Brazil and now has plans to launch in countries across Latin America.

This newsletter is brought to you by:

🚀 Alpha Tournament: Today is the last day to register for Season 13! Make sure you claim your seat and build your portfolio before 11:59PM ET tonight.

—

🧑💻 Alpha Vantage provides enterprise-grade financial market data through a set of powerful and developer-friendly APIs. From traditional asset classes (e.g., stocks and ETFs) to economic metrics, from foreign exchange rates to cryptocurrencies, from fundamental data to technical indicators, Alpha Vantage is your one-stop shop for real-time and historical global market data delivered through RESTful stock APIs, Excel, and Google Sheets.

Earnings Reports 💰

Disney ($DIS)

Revenue: $21.5B vs $20.1B expected and $17.0B year ago (+26% YoY)

EPS: $1.09 vs $0.96 expected and $0.80 year ago (+36% YoY)

Op. Income: $3.6B vs $2.4B (+50% YoY)

Disney+ Subs: 152.1M vs 147.8M expected and 116M year ago (+31% YoY)

Guidance: Lowered its 2024 forcast for Disney+ subs to 215M - 245M, down from previous guidance of 230M - 260M

Important Notes: Total platform subscriber base (Disney+, ESPN+, and Hulu) of 221M now suprases that of Netflix’s 220.7M subscribers. Disney also announced an ad-supported plan for Disney+ to be released in December. Parks segment revenue grew 70% YoY to $7.4B

Market Reaction (24hrs after report): +4.7%

—

Coinbase ($COIN)

Revenue: $808M vs $832M expected and $2.23B year ago (-63.8% YoY)

EPS: ($4.98) vs ($2.65) expected and $6.42 year ago

Monthly Transacting Users (MTUs): 9M vs 8.8M year ago (+2.3% YoY)

Trading Volume: $217B vs $462B year ago (-53.0% YoY)

Assets on Platform: $96B vs $180B year ago (-46.7% YoY)

Transaction Revenue: $655M vs $1.93B year ago (-66% YoY)

Guidance: FY’22: 7M-9M MTUs, ARPU in low ~$20 range, subscription & services revenue >$600M, reduced guidance for SG&A expense to $4-$4.25B from $4.25-$5.25B

Important Notes: Of the $217B in trading volume, 21% was from retail and 79% was from institutions. However, of the $655M in transaction revenue, 94% was generated by retail and 6% was generated by institutions. Coinbase reduced its headcount by 18% in June (~1,100 employees)

Market Reaction (24hrs after report): +7.4%

—

Palantir ($PLTR)

Revenue: $473M vs $471M expected and $375.6M year ago (+25.9% YoY)

EPS: ($0.01) vs $0.03 expected and $0.04 year ago

Adj. Op. Income: $108M vs $117M year ago (-7.7% YoY)

Government Revenue: $263M vs $232M year ago (+13% YoY)

Commercial Revenue: $210M vs $144M year ago (+46% YoY)

Guidance: Q3 revenue $474 - $475M and adj income of $54 - $55M. FY’22 revenue ~$1.9B and adj income of $341 - $343M

Important Notes: Added 27 new customers in Q2, bringing their total to 304 customers (+80% YoY). Ended the quarter with $3.5B in remaining deal value.

Market Reaction (24hrs after report): -14.2%

Week Ahead 📅

Monday

NAHB Home Builders Index (exp. 54)

Earnings Reports: Nu Holdings ($NU)

Tuesday

Housing starts (exp. 1.5M)

Building permits (exp. 1.7M)

Earnings Reports: Walmart ($WMT), Home Depot ($HD), Sea Ltd ($SE)

Wednesday

Retail sales (exp. +0.1%)

Business inventories (exp. +1.4%)

Earnings Reports: Cisco Systems ($CSCO), Lowe’s Corp ($LOW), TJX Companies ($TJX), Target ($TGT), Synopsys ($SNPS)

Thursday

Jobless claims (exp. 265K)

Phili Fed Manufacturing Index (exp. -4.5)

Existing home sales (exp. 4.8M)

Earnings Reports: Estee Lauder ($EL), Applied Materials ($AMAT), Net Ease ($NTES), Bill,com ($BILL),

Friday

Earnings Reports: Deere & Co ($DE)

Did you like this Sunday Market Newsletter? Consider sharing it!

Until next Sunday…